America’s semiquincentennial would be a sad and grudging affair without a nod to the nation’s founding capitalists. Robert Morris, the “Financier of the Revolution,” donated his own fortune to supply the raggedy and underpaid armies of George Washington. George F. Baker sold the bonds that raised the money that equipped the Union side in the Civil War. Along with the statesmen and the generals and the keepers of the home fires, the moneybags deserve their day in the sun, too.

Morris and Baker were rich, bold, indomitable, enterprising, self-made, proficient, cool in a crisis, and incapable of despair. Each was an unshakable optimist on the American future. “While you may make many mistakes,” J.P. Morgan’s father advised his son, “never be a bear on your country or you will surely go broke.” Baker, who heard the story directly from the younger Morgan, was always a bull, too. Morris, who died in 1806, seven years before the birth of the elder Morgan, was no less an optimist. Indeed, Morris’s heavily encumbered purchases of millions of acres of American wilderness in the 1790s ultimately cost him his fortune.

Historians have thought the less of Morris for dying broke, but the financier was a nonpareil, rich or poor: successful merchant and ship owner; early opponent of overbearing British colonial rule; tireless advocate of American independence; logistical, commercial, and maritime genius of the Second Continental Congress. “For three critical months in the winter of 1777,” wrote his biographer, Charles Rappleye, “when Congress fled Philadelphia for the relative safety of Baltimore, Morris ran the operations of the American government virtually single-handed.”

The one-man government retired from the Continental Congress in 1778, but in 1781 he became the Superintendent of Finance—in effect, the secretary of the treasury of the revolutionary government, though of treasure the infant nation had none. Lacking the power to tax, the national government could only appeal. Morris begged and requisitioned the states but to no avail; Massachusetts, Rhode Island, and Maryland proving especially recalcitrant. He therefore improvised. He hired an engraver, procured copper plates, and printed his own currency—“Morris notes”—which, in testament to their originator’s good name, passed for money in the rebellious colonies. “My personal credit, which thank Heaven I have preserved through all the tempests of the War,” the superintendent advised a friend, “has been substituted for that which the Country has lost. I am now striving to transfer that Credit to the Public.”

To fill the credit void, Morris also founded the Bank of North America, the nation’s first commercial bank. His creation would take deposits, including the government’s. It would lend to the government and private business alike. Its officers would receive no remuneration except that which the stockholders voted them (the offices in Morris’s bank would be those of honor, not profit). As for the currency of the Bank of North America, a citizen could take it or leave it. Morris was as dead set against legal tender laws (which compel a creditor to accept the government’s money in payment of a debt) as he was against price controls. As he wrote to John Jay on July 13, 1781, he envisioned a bank “to unite the several states more closely together in one general money connection and indissolubly to attach many powerful individuals to the cause of their country by the strong principle of self-love and the immediate sense of private interest.” The bank, its founder expected, would become a permanent “Pillar of American Credit.”

Morris saw the enabling legislation through the Continental Congress and was on hand the day the bank opened—January 7, 1782—to borrow $100,000 in the name of Michael Hillegas, the first Treasurer of the United States. Morris was the bank’s largest stockholder—except for a brief moment late in 1782 when John Paul Jones invested his prize money. The Bank of North America paid high dividends from the start. It proved the predecessor to Alexander Hamilton’s Bank of the United States (established in 1791) and distant forebear of the Federal Reserve (established in 1913), whose interest-rate manipulations and fast-paced money printing would have left Morris, a gold-standard man, dumbfounded.

Success earned Morris not only acclaim, but also resentment and brickbats (“pecuniary dictator,” a detractor sneered). The superintendent amiably suffered his critics. “[A]ny abuse or misrepresentation which particular persons may indulge themselves in I consider the necessary trappings of office,” he told a correspondent in 1782, “and if they can obtain forgiveness from their country they will always have mine most freely.”

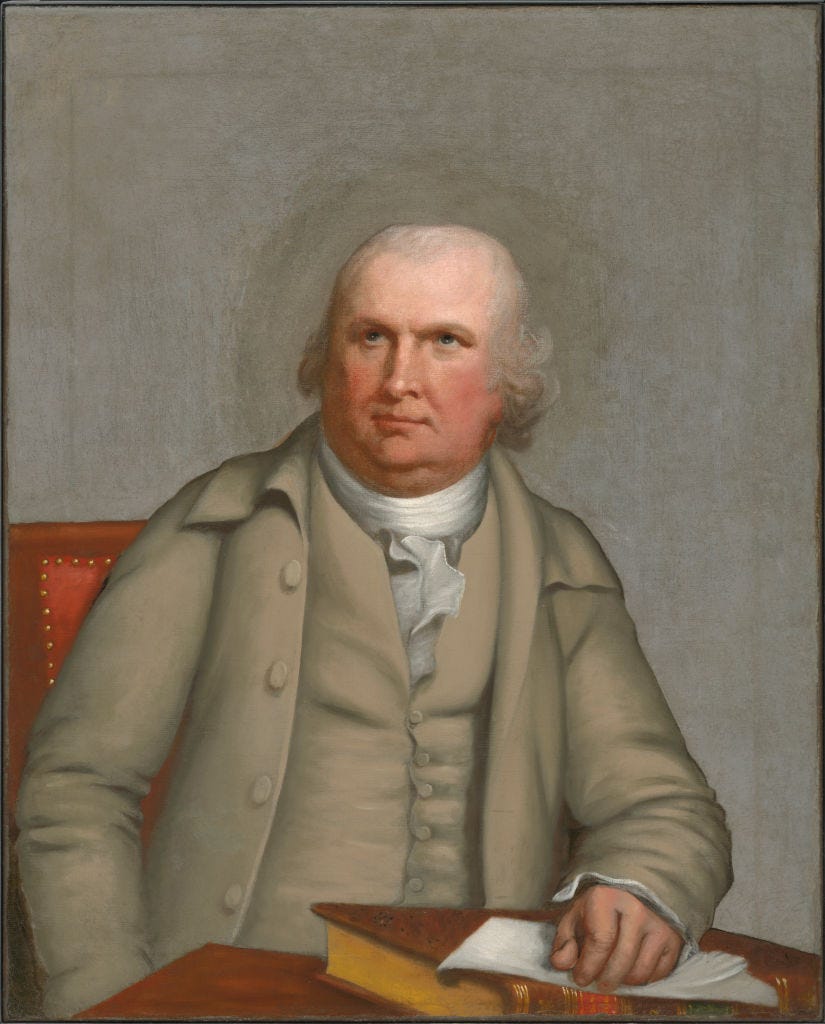

Sitting for his portrait a few years later, Morris presented the artist, Robert Edge Pine, with a broad determined face, a receding hairline (the subject was 51 years old), and exactly the boldness required of anyone who would amass $3 million of unrepayable debt in the course of conducting speculations in millions of virgin acres in Pennsylvania, Virginia, Georgia, and the Carolinas (as well as 7,234 building lots in the brand new District of Columbia).

From debtors’ prison in 1798, eight years before his death, Morris gently deflected an importuning creditor: “I wish you would not write to me in such terms as you do. You wound me to the soul, and if that does you any good I will submit patiently, but if it does not ease you why wound me deeply when my most ardent wish is to relieve you?”

An old banker’s death led the front page of The New York Times on Sunday, May 3, 1931. The 1929 crash had long since knocked the banking profession off its bull-market pedestal, but the Times still made pride of place for a eulogy of George F. Baker.

He was the “dean of American bankers.” When he was a young man, Baker could perform one-arm pull-ups. As an old man, with his silver muttonchop whiskers and black top hat, regally seated in his custom Pierce-Arrow town car (the elevated roof of which accommodated the banker’s hat), he might have inspired the creators of the Monopoly game’s Rich Uncle Pennybags. His blue eyes welled with tears whenever he recalled the assassination of Abraham Lincoln.

A philanthropist and investor, Baker was president of the First National Bank of New York at the corner of Broadway and Wall Street. Federally uninsured, lightly regulated, and by no means too big to fail, the First was an institution that harked back to Alexander Hamilton’s time as much as it anticipated our own. Some judged the First to be impregnable, and, indeed, the Bank of England chose it over the Federal Reserve Bank of New York as the safest institution in which to place a large deposit in the darkest days of the Great Depression.

Morris and Baker were rich, bold, indomitable, enterprising, self-made, proficient, cool in a crisis, and incapable of despair.

Baker, born in 1840, was 23 when he joined the newly organized First National Bank and 33 in the year of the panic that ruined Jay Cooke and the Union Pacific Railroad, and threatened every New York City bank, not excluding the First. What should we do if frightened depositors came running? Baker was asked. “Pay every claim presented as long as the money lasts,” the stout young man declared. “When we stop paying it will be because there is not another dollar in the till, and none obtainable.” The First survived and Baker, within four years, was its president.

The First was a moneymaking hybrid, unusual for its time and extinct today, thanks to federal banking regulations: part investment bank, part venture capitalist fund, part bond-trading house, and part commercial bank. The bank was engaged, in the words of a starstruck federal bank examiner, “in many undertakings of that character which generally turn out favorably.”

And in the words of another federal examiner, circa 1877, concerning the First’s $2 million infusion of emergency aid in a needy Rochester bank: “[T]here is not a single Bank in our City who would or could have helped a country correspondent to such gigantic figures and on such short notice!” And during the long-lingering depression of 1873–79 to boot.

Baker accumulated directorships, wealth, and accolades. From the April 14, 1924, edition of Time magazine: “True, he is twice as rich as the original J.P. Morgan, having a fortune estimated at 200 millions. True, at the age of 84 when he has retired from many directorates, he dominates half a dozen railroads, several banks, [and] scores of industrial concerns.” The banker donated $5 million to the founding of the Harvard Business School, $2 million to Cornell University, and $1 million to the Metropolitan Museum of Art. He is the namesake of the Baker Memorial Library at Dartmouth College (expanded in 2002 to become the Baker-Berry Library).

A bull “who always bought and very rarely sold,” Baker showed best in a crisis. The bank and the nation always snapped back from panics and depressions, even the close call of 1873, stronger than before. Surely, he reasoned, the post-1929 slump would prove no different.

His younger colleagues were not so sure, and they begged him to reduce the bank’s exposure to the overvalued stock market. Baker turned a deaf ear and went into the crash fully invested, a decision that sawed his peak net worth in half. “I was a damn fool,” his biographer, Sheridan Logan, quotes Baker as saying at some post-crash low moment, though who, no matter how deep-rooted his faith in the American future, wouldn’t have at least thought it in 1930?

Even so, his Wall Street admirers agreed: The famously lucky banker had salvaged a kind of victory even from that unforced error. Dying at a low ebb in the stock market, he lightened his heirs’ estate-tax liability.

“His death,” said The New York Times, “leaves only John D. Rockefeller Sr. to represent the leaders of an era that saw the passing of the last frontier and the flowering of a new civilization which they and their contemporaries helped to build.” The Times’ article cast no political aspersions on the capitalist’s substantial remaining wealth, still less on his faith in the market system, and praised his contributions to the making of modern America: “Although Mr. Baker’s chief interest was in banking and finance, he was among the group which in the last century flung rails of steel across the continent and helped this nation prepare for the transition from an agrarian age to one of machines and mass production.”

America today is rich beyond imagining. The sky-high level of household net worth expressed as a percentage of gross domestic product only confirms what the untrained eye can see. For the owners of stocks, bonds, and houses, these are the good old days, gasoline prices and political fracturing (and, yes, elevated valuations and heavy indebtedness) notwithstanding. Baker, the beau ideal of the banker-cum-investor, and Morris, the avatar of the patriot financier, set posterity brave and inspiring examples.

A Gilded Age contemporary of Baker’s, George G. Williams, president of the Chemical National Bank, left a legacy in four words. The Chemical had earned for itself the moniker “Old Bullion” for faithfully paying out gold coin to nervous depositors in the Panic of 1857. Like Baker, Williams had managed to combine profits and safety in the inherently risky business of lending and borrowing. Asked for the secret of his decades-long success, the banker replied, “The fear of God.”

The Free Press earns a commission from any purchases made through all book links in this article.

Thank you for reminding us of the untold heroes who financially were more concerned in the rescue of the Republic than in their own fortunes. I knew of Morris, but not of Baker.

Been reading Jim for 40 years. Glad to see him on TFP.